Summer is finally here and there’s nothing quite like LA in the summer! Work hard, play harder - but the question is how… Here are some of my top picks:

LA Happenings: 9 & 10 July

2022 - 2023 Luxury Housing Forecasts

It seems like just about everything is rising whether it’s gas prices, inflation, or mortgage rates. It’s a lot to deal with, but the housing forecasts for 2022-2023 will hopefully bring some hope and some relief. Case in point, it is forecasted that mortgage rates will start to decrease after this quarter. Additionally, home prices growth rates will start to decrease after this quarter and continue to decrease for the foreseeable future.

As for the million-dollar question, will the housing inventory catch up to the demands? It’s not as simple to answer as there are so many affecting factors. Read on to find out the important housing forecasts of 2022-2023.

MORTGAGE RATES

Mortgage rates have been on the increase since 2021, but within the past 5 months, the mortgage rates have shot up by over 2%. This is due to the Federal Reserve’s attempt to counter the current inflationary pressures with multiple interest rate increases. As a result, the mortgage rates are the highest they’ve been all year. As evidenced from the above graph, the current 30-year fixed mortgage rate is 5.78% and is a result of a high spike from late 2021. However, the mortgage rates are expected to decrease over the next few years as the higher rates are expected to price out some home buyers, and ideally decrease the demand for houses.

In fact, it’s predicted that the 30-year fixed mortgage rate will decrease from 5.2% to 5.0% at the end of 2022 and 4.8% at the end of 2023 according to the Mortgage Bankers Association (MBA). It is the hope that the buyer demand for houses will fall, and give opportunity for the housing supply to increase to bring more balance to the housing market.

To recap, the increased mortgage rates will slow the housing sales, and result in lower mortgage rates in 2023.

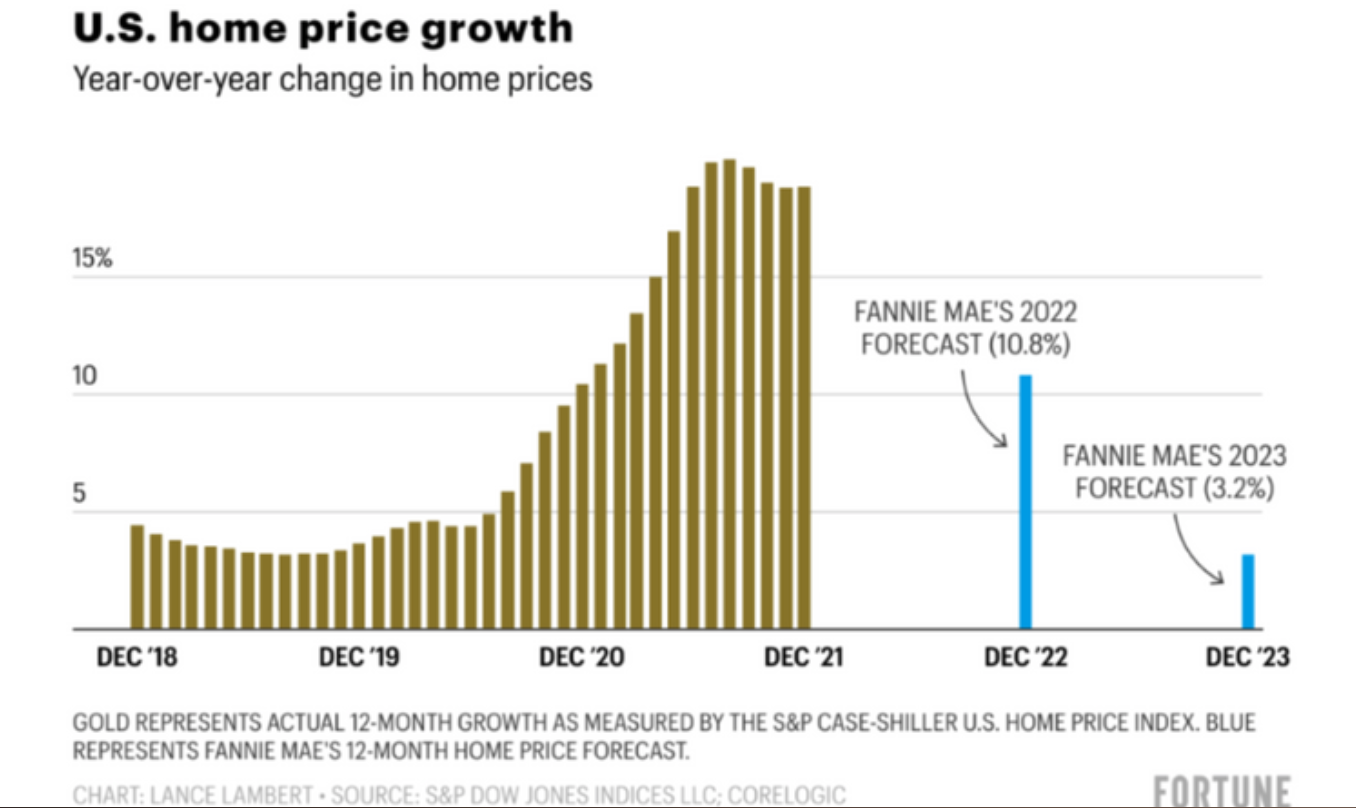

HOME PRICES

Since 2020, home prices have dramatically increased nationwide as shown in the graph above, but it is forecasted to decrease to 10.8% at the end of 2022 and 3.2% in 2023. The demand for housing since the pandemic has shot up, but the pandemic and other factors have caused the supply of houses to fall far behind. As a result of this, housing prices have been on the rise with some buyers paying way more than the asking price of a house. In fact, Los Angeles’ median home price was $998K, a far cry from the national average median home price of $428,700.

“THE DEMAND FOR HOUSING SINCE THE PANDEMIC HAS SHOT UP, BUT THE PANDEMIC AND OTHER FACTORS HAVE CAUSED THE SUPPLY OF HOUSES TO FALL FAR BEHIND”

However, compared to other states, California didn’t have such a drastic home price growth rate. For example, the year-over-year home price growth rate for California was 5.6% as shown in the graph below, whereas the national year-over-year home price growth rate was 20.9%. This could be due to the “California Exodus,” as well as the work-from-home trend causing prospective homebuyers to move to lower priced areas, like Arizona and Utah, since there is no need to be in close proximity to work. However, with increased mortgage rates pricing out a portion of prospective homebuyers, the forecast is that home price appreciation will plunge to single digits again.

To conclude, increased mortgage rates will halt and price out potential home buyers, which will slow the rate of home sales. This will lead to buyer demand for houses slowing, and bring the home price appreciation rate to a low number by 2023.

To conclude, increased mortgage rates will halt and price out potential home buyers, which will slow the rate of home sales. This will lead to buyer demand for houses slowing, and bring the home price appreciation rate to a low number by 2023.

HOUSING INVENTORY

California, and the rest of the United States, is currently experiencing a Seller’s Market. The shortage of housing inventory with the high demands of houses works in the seller’s favor, resulting in increased home prices and houses selling quickly. The factors affecting the low supply in housing include the COVID pandemic, high costs of supplies (think lumber and windows), and overworked construction workers falling behind on schedule to keep up with housing demands.

While the active listings are drastically low compared to housing demands, there was a slight increase in

March for active listings, making it the first year-over-year gain since June 2019. Newly added listings also increased for the first time since August 2021, and the month-to-month increase of 37.7% in newly added listings was also the highest its been since May 2020. While it’s optimistic news that active listings finally rose, the housing supply is still moving rather slowly. However, it should be noted that the existing-home

sales in the West decreased 5.8% in April compared to the previous month, and decreased 2.4% nationally in April. To put it in perspective just how low the housing inventory is in Los Angeles, the Months Supply of Inventory (MSI) is 1.8 months, whereas a balanced market would have a number between 4 and 6 months. MSI calculates the relationship between supply and demand in a housing market. With the increase in new listings and the decrease in existing-home sales, the idea is that the housing supply should have a chance to slowly creep back up, but expect it to be a seller’s market for a bit.

“NEWLY ADDED LISTINGS ALSO INCREASED FOR THE FIRST TIME SINCE AUGUST 2021, AND THE MONTH-TO- MONTH INCREASE OF 37.7% IN NEWLY ADDED LISTINGS WAS ALSO THE HIGHEST ITS BEEN SINCE MAY 2020”

To sum up, if the buyer demand for housing slows as forecasted, it will allow for the housing inventory to have a chance to slowly catch up. Will it ever surpass demand? Most likely not, but it should bring more of a balanced housing market for 2023.

CONCLUSION

In the time it took to read this, the mortgage rates have most likely increased, but maybe it will bring us one step closer to a more balanced housing market. The forecast does show a much lower mortgage rate by the end of the year and by 2023. Additionally, the home price appreciation growth rate is expected to slow drastically, which will normalize the housing market and should work in the buyer’s favor.

The most concerning point of all, housing inventory should be expected to increase, albeit at a crawling pace.

The factors of existing-home sales decreasing, newly added listings increasing and high mortgage rates should all work together to bring balance to the housing market.

SOURCES

https://www.freddiemac.com/research/forecast/20220418-quarterly-forecast-purchase-market-will-remain-solid-even-mortgage-rates-rise

https://www.freddiemac.com/pmms

https://www.mba.org/docs/default-source/research-and-forecasts/forecasts/mortgage-finance-forecast-may-2022.pdf?sfvrsn=c2d57ab9_1

https://www.noradarealestate.com/blog/california-housing-market/ https://www.nar.realtor/newsroom/existing-home-sales-retract-2-4-in-april https://www.noradarealestate.com/blog/los-angeles-real-estate-market/#Los_Angeles_County_Housing_Market_Trends

https://fortune.com/2022/04/21/zillow-cuts-its-housing-market-and-home-price-forecast-for-2022-and-2023/ https://www.realtor.com/realestateandhomes-search/Los-Angeles_CA/overview https://www.inman.com/2022/04/19/modest-recession-eyed-in-2023-fannie-mae-economists-predict/ https://fred.stlouisfed.org/series/MSPUS

https://www.corelogic.com/intelligence/u-s-home-price-insights/

LA Happenings: 2 - 4 July

LA Happenings: 25 & 26 June

Luxury buyers desire homes that are smart & safe for family and planet

Luxury homebuyers have always been particular about what they’re looking for in their next home purchase but periodically the top priorities for their key amenities and features shift. In the latest report from Luxury Portfolio International, based on high net worth consumers are turning more and more of their focus towards safety and sustainability.

LA Happenings: 18 & 19 June

Are online home estimations accurate?

Barely a day goes by that a client brings up the ‘Zestimate’ or ‘Redfin Estimate’ of their home and my word is it a pet peeve of mine… Made popular by sites such as Zillow, Redfin, and Trulia, online estimates seek to provide the client with what their home is worth. The convenience is undeniable, but the same can’t be said about the accuracy.